Are You Building for the India That's Coming?

A note for CEOs, MDs, and Board Leaders of India’s growth-stage and enterprise companies

India’s GDP is set to rise from USD 4.18 trillion today to USD 30 trillion by 2047.

That is not a government headline. That is the most consequential structural fact your organization needs to plan around right now.

NITI Aayog’s landmark study, Scenarios Towards Viksit Bharat and Net Zero, published in 2026, models what this transformation actually looks like sector by sector, decade by decade. And if you read it as a CXO, one thing becomes immediately clear: the companies that will lead in 2035 are making decisions in 2026 that most of their peers have yet to schedule into a strategy review.

What Viksit Bharat Actually Means for Your Business

The popular framing of Viksit Bharat is aspirational. The NITI Aayog modelling, however, is clinical. It tells you precisely what happens to demand, supply chains, labour markets, and capital costs as India converges toward developed-economy status.

Here is what the numbers say by 2047:

- India’s urban population rises from 37% to 51%, generating unprecedented demand for housing, mobility, services, and energy

- Steel demand grows from 127 million tonnes to 568 million tonnes

- Cement demand rises from 391 MT to 1,471 MT

- Passenger transport demand more than triples

- AC penetration leaps from 10% of households to 65%

- Farm mechanisation reaches 100%

This is not incremental growth. This is a structural reshaping of the Indian economy within a single leadership generation.

The companies supplying these markets and the companies served by these supply chains are entering a period where strategy cycles of three to five years are dangerously short.

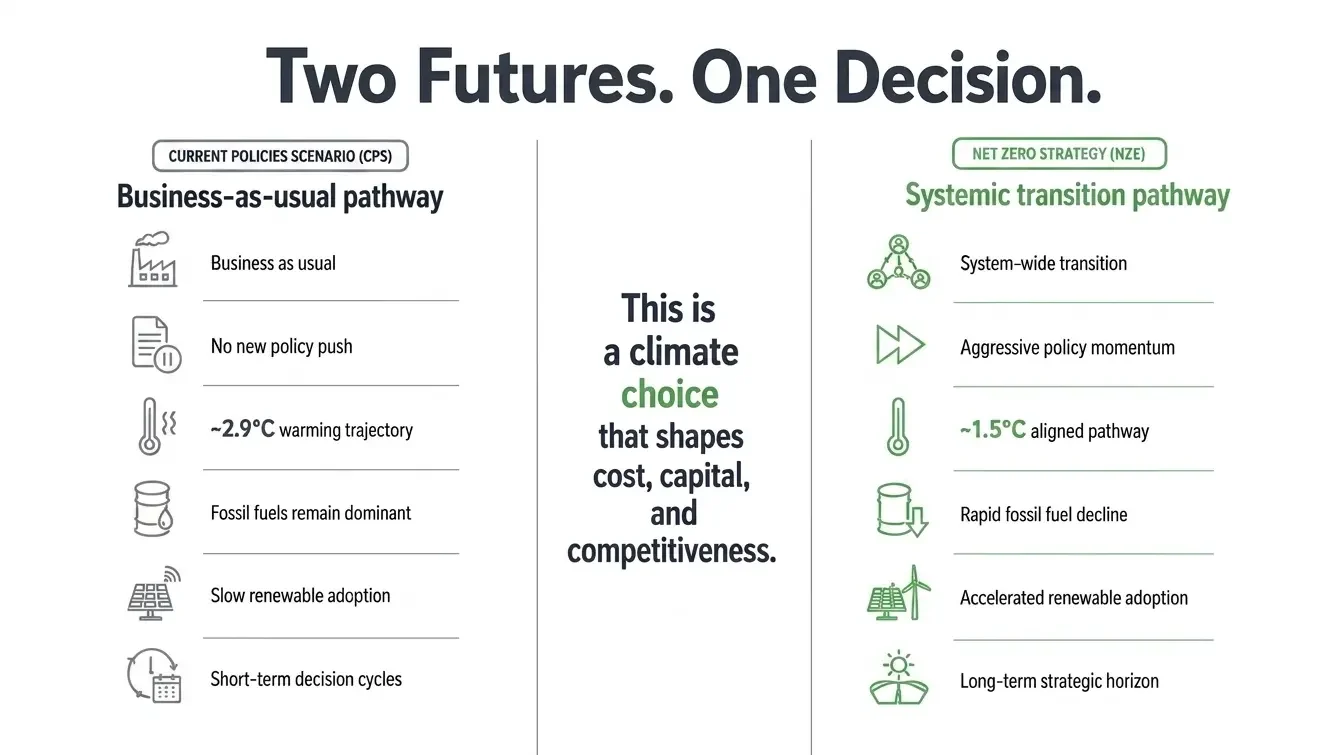

Every point of GDP growth in India’s next chapter requires more energy. Final energy demand is projected to grow 2.1 to 2.6 times by 2070. Electricity consumption alone is expected to rise 6 to 8 times over 2025 levels.

But here is the strategic insight that most leadership teams are missing: the composition of that energy is changing just as dramatically as the quantity.

In the Net Zero Scenario, renewable energy’s share in primary energy rises from 3% in 2025 to 63% by 2070. Fossil fuels fall from 87% to 14%. Demand electrification, the share of electricity in final energy use doubles from 21% to 60%.

For CXOs, this is a cost structure and a capital allocation story. It is a supply chain resilience story. The organisations that lock in long-term renewable energy agreements now, that electrify industrial processes ahead of regulatory compulsion, that integrate energy procurement into their five-year capex cycles, these organizations are making tomorrow’s cost structure today’s advantage.

Three Strategic Questions Your Next Board Meeting Should Answer

1. Is your growth model calibrated to the new India or the old one?

The urbanisation surge, the infrastructure buildout, the expansion of the consuming middle class create genuine tailwinds. But they also create resource intensity challenges: land, water, skilled labour, and energy are all under pressure. Companies that have explicitly mapped their growth strategy against India’s structural transformation are fundamentally better positioned than those waiting for the opportunity to become obvious.

2. Have you mapped your exposure to transition risk?

CBAM – Europe’s Carbon Border Adjustment Mechanism is already live, with global supply chains beginning to price carbon. As India’s own regulatory environment tightens, and as export markets demand verified sustainability credentials, the carbon intensity of your operations will affect your market access and your valuations.

3. Are you treating sustainability investment as CapEx or as strategy?

The distinction matters enormously. CapEx thinking produces minimum-compliance behaviour. Strategic thinking produces competitive positioning. Leading Indian and global companies are treating energy transition not as a cost to be managed but as a source of structural advantage to be captured.

The companies that moved early on digital infrastructure in 2010 did not just gain an IT advantage. They gained an organisational capability advantage that has compounded for fifteen years. The energy and sustainability transition offers a structurally analogous opportunity.

The window to act ahead of regulatory mandates, ahead of full market pricing of carbon, and ahead of supply chain restructuring is open. The NITI Aayog modelling makes clear that the transition happens regardless. What remains a choice is whether your organisation leads it or follows it.

Related posts